If you have cash sitting in a savings account earning 0.5% APY, you're leaving money on the table. A CD ladder strategy can earn you 4–5× more interest while keeping your money accessible on a predictable schedule.

Here's exactly how it works, how to build one, and how to calculate your earnings.

What Is a CD Ladder?

A CD ladder is a savings strategy where you split your money across multiple certificates of deposit with staggered maturity dates. Instead of locking all your money in one CD for 5 years, you spread it across CDs that mature at different intervals.

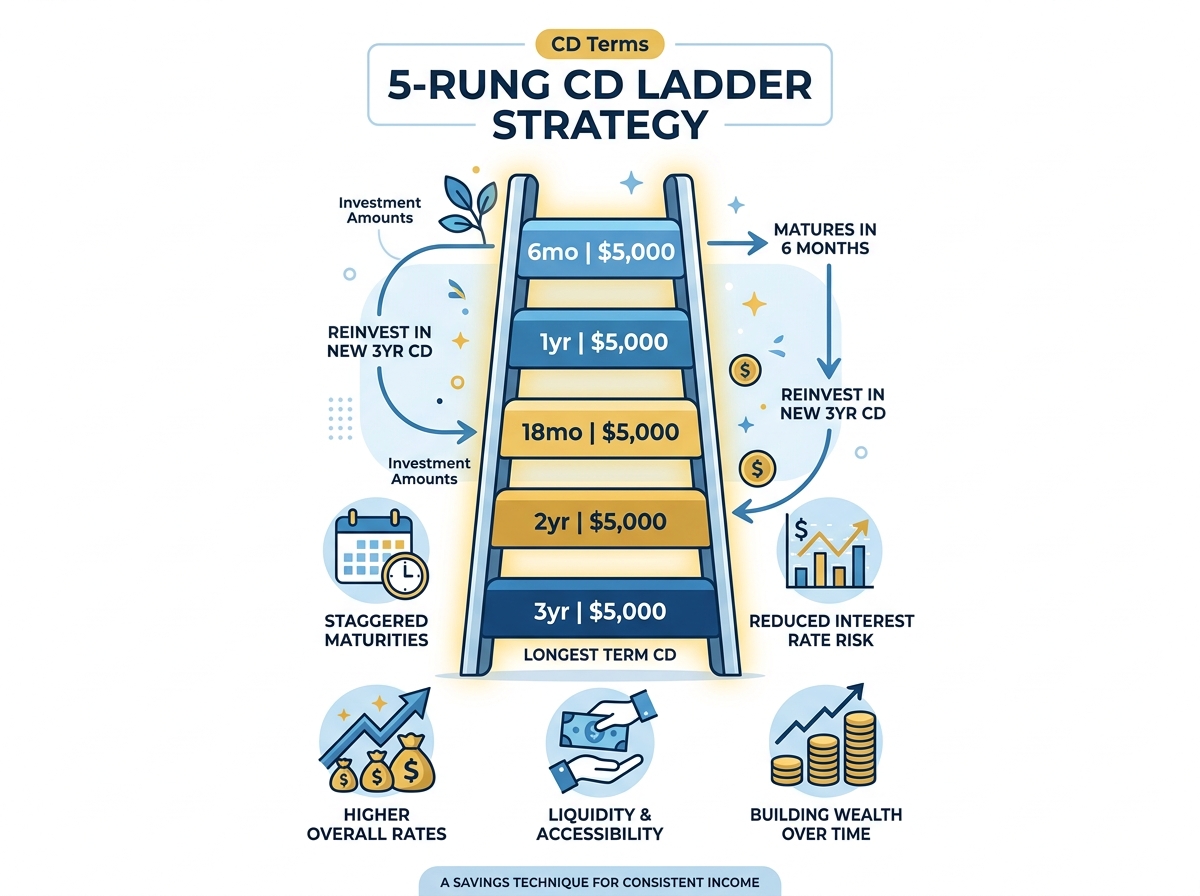

How It Works: A 5-Rung Example

Let's say you have $10,000 to invest. Here's how a 5-rung CD ladder works:

| Rung | Amount | Term | APY (2026) | Maturity |

|---|---|---|---|---|

| 1 | $2,000 | 6 months | 4.50% | Dec 2026 |

| 2 | $2,000 | 1 year | 4.75% | Jun 2027 |

| 3 | $2,000 | 18 months | 4.60% | Dec 2027 |

| 4 | $2,000 | 2 years | 4.40% | Jun 2028 |

| 5 | $2,000 | 3 years | 4.25% | Jun 2029 |

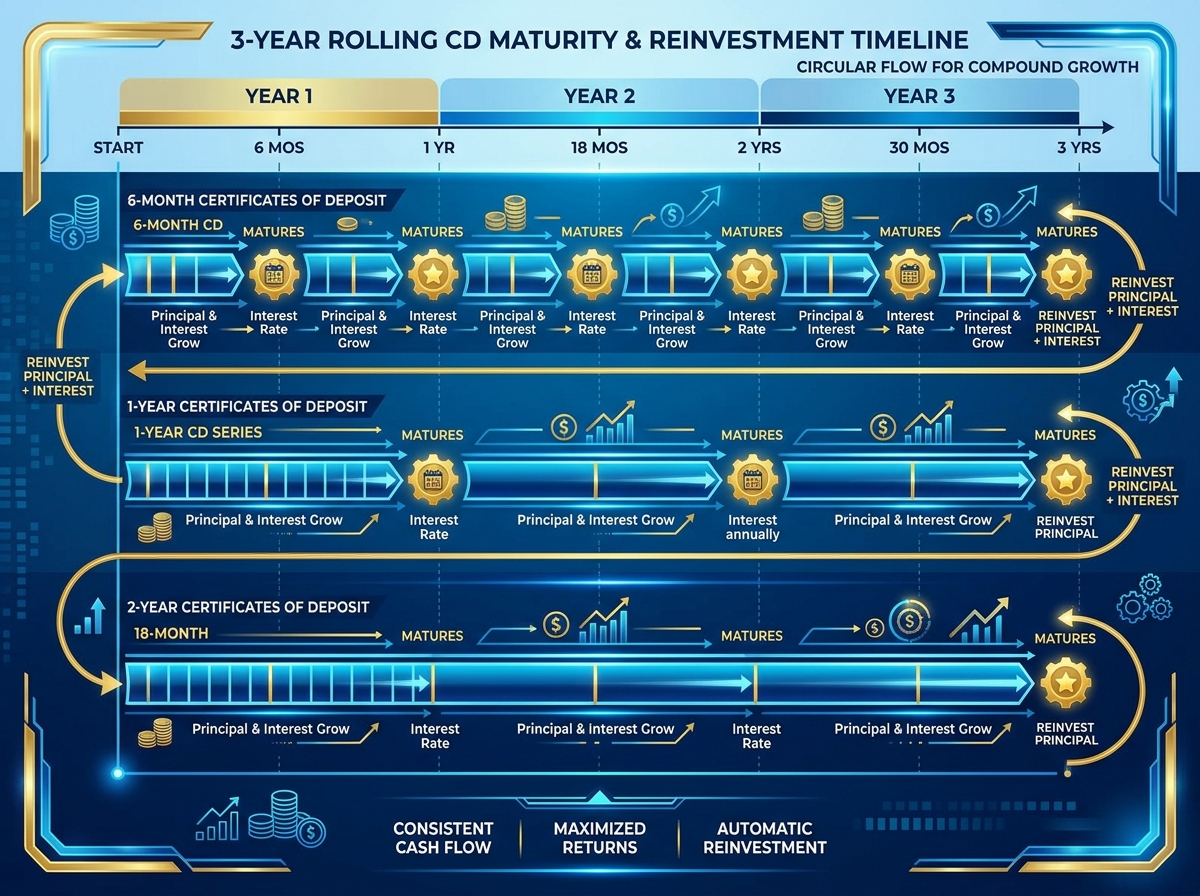

When rung 1 matures in December, you reinvest it at the best available 3-year rate. When rung 2 matures, same thing. You keep rolling forward, always earning top rates while having money coming due regularly.

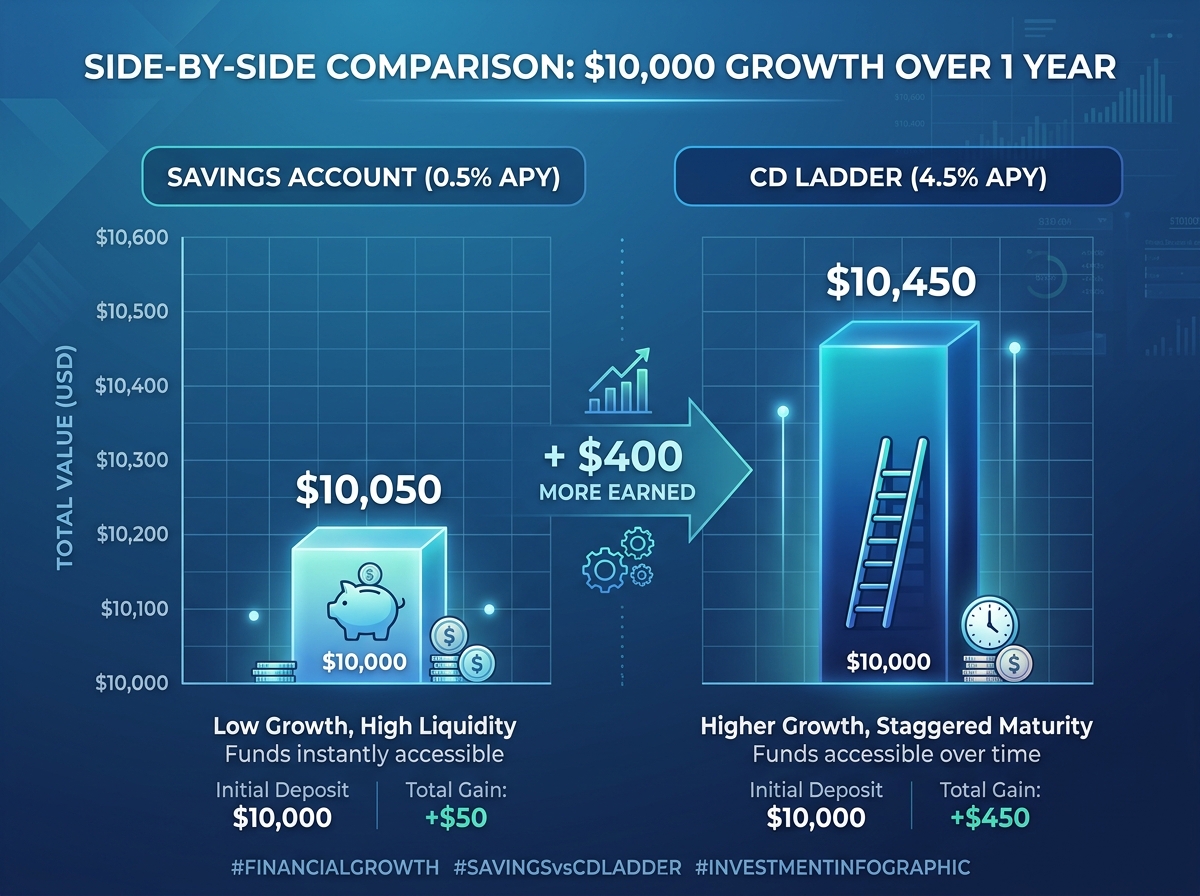

CD Ladder vs Savings Account

| Feature | Savings Account | CD Ladder |

|---|---|---|

| APY (2026 avg) | 0.4% – 0.6% | 4.25% – 5.00% |

| $10,000 earns in 1 year | $40 – $60 | $425 – $500 |

| Liquidity | Instant access | At maturity dates |

| Penalty for withdrawal | None | 3–6 months interest |

| Rate guarantee | Variable, can change | Fixed for term |

| FDIC insured | Yes (up to $250K) | Yes (up to $250K) |

A CD ladder earns 7–10× more than a typical savings account while still giving you periodic access to your cash.

Use Our Free CD Ladder Calculator

Build your custom CD ladder and see exactly how much interest you'll earn over time.

CD Ladder CalculatorHow to Build Your CD Ladder

This is the total amount you want to put into CDs. Most banks require a $500–$1,000 minimum per CD.

3–5 rungs is standard. More rungs = more liquidity but slightly more complexity.

Divide your total by the number of rungs. Each rung gets an equal amount.

Purchase CDs so each matures 6–12 months apart. Start with the shortest term.

When a CD matures, reinvest it into a new CD with the longest term in your ladder.

Current CD Rates (June 2026)

| Term | Top Rate | Average Rate | Best For |

|---|---|---|---|

| 3 months | 4.75% | 4.20% | Emergency fund ladders |

| 6 months | 5.00% | 4.50% | Short-term savings |

| 1 year | 5.10% | 4.75% | Medium-term goals |

| 18 months | 4.90% | 4.60% | Balanced approach |

| 2 years | 4.75% | 4.40% | Goal-based saving |

| 3 years | 4.60% | 4.25% | Long-term locking |

| 5 years | 4.50% | 4.10% | Maximum yield |

CD Ladder Variations

3-Rung Ladder (Simple)

Best for beginners. Split $6,000 into three $2,000 CDs: 6-month, 1-year, and 2-year. Total first-year interest: ~$270.

5-Rung Ladder (Standard)

Best balance of yield and liquidity. Split $10,000 into five $2,000 CDs: 6-month through 3-year. Total first-year interest: ~$460.

Barbell Strategy

Split between short-term (3-month) and long-term (5-year) CDs. You get quick access to some money plus maximum yield on the rest.

Tax Considerations

CD interest is taxed as ordinary income at your federal tax rate. If you're in the 22% bracket and earn $460 in CD interest, you'll owe about $101 in federal tax.

Frequently Asked Questions

What if I need my money before the CD matures?

You'll pay an early withdrawal penalty — typically 3–6 months of interest for shorter terms and up to 12 months for longer terms. Some banks offer "no-penalty" CDs with slightly lower rates.

How much do I need to start a CD ladder?

Most banks require $500–$1,000 minimum per CD. A 5-rung ladder needs $2,500–$5,000 minimum. Some online banks have no minimum.

Are CDs better than high-yield savings accounts?

CDs earn more (4–5% vs 0.5%), but you lock your money for the term. If you need instant access, use a high-yield savings account. For money you won't need for 6+ months, CDs win.

What happens when a CD matures?

The bank typically auto-renews at the current rate (often lower). Set a reminder to reinvest manually into a new CD at the best available rate.

Can I add money to a CD after opening it?

Generally no — CDs are fixed deposits. If you want to add regularly, open a new CD at each maturity and add your new savings to it.

What's the best CD ladder for retirees?

A 3-rung ladder (3-month, 6-month, 1-year) provides regular income with higher rates. Reinvest each CD as it matures for rolling income.